Most people earn money. But far fewer know how to manage it properly. You might pay your bills, enjoy the occasional treat, or even put away some savings—but have you ever paused to consider where you stand financially, long-term?

Are you overspending without realizing it?

Do you know your financial goals—and more importantly, do you know how to reach them?

If these questions make you uncomfortable, don’t worry. You’re not alone.

That’s why understanding the personal finance basics is so crucial. Financial literacy is more than just knowing how to save money—it’s about gaining control over your present and securing your future. With a few practical habits, anyone can build a solid financial foundation.

Let’s dive into the essential principles that can change the way you view and manage money.

What Is Personal Finance, Really?

At its core, personal finance is about how you manage your money across every stage of your life. It includes budgeting, saving, borrowing, investing, and preparing for retirement. It’s about understanding your income, your spending habits, and the goals you set for your financial life.

The idea isn’t just to avoid debt—but to actively build wealth, however modestly. That could mean saving for your child’s education, buying your first home, or launching an eco-friendly building business that aligns with your values.

Personal finance empowers you to make these goals achievable, no matter your income level.

Step 1: Define Your Financial Goals

The first and most essential step is knowing what you want. Financial freedom looks different for everyone. Maybe you want to retire early. Or buy a cabin in the mountains. Or simply be able to sleep soundly at night, knowing your bills are paid.

The clearer your goal, the more actionable your plan becomes. A vague goal like “I want to be rich” won’t help. Instead, define your aims with specifics:

- “I want to pay off my credit card in 6 months.”

- “I’ll save $5,000 this year for an emergency fund.”

- “I want to invest 15% of my income every month.”

Your goals should be realistic, trackable, and time-bound. Without a target, even the best financial advice won’t lead anywhere.

Step 2: Build and Use a Budget

Budgeting is the heartbeat of personal finance. It’s how you measure your financial reality against your financial intentions.

A simple monthly budget includes:

- Your income: salary, freelance work, passive earnings

- Fixed expenses: rent, utilities, subscriptions

- Variable expenses: food, fuel, entertainment

- Savings & investments: emergency funds, retirement, etc.

Apps like You Need A Budget or even a basic spreadsheet can help track your spending. The goal isn’t restriction—it’s awareness. Once you see where your money actually goes, you gain power over it.

Budgeting gives you permission to spend confidently—guilt-free—on what matters to you most.

Step 3: Create an Emergency Fund

Life is unpredictable. Job loss, medical emergencies, sudden car repairs—they happen when you least expect it. That’s why building an emergency fund is non-negotiable.

Aim for 3–6 months’ worth of essential living expenses saved in a separate, easily accessible account. It won’t happen overnight, but contribute regularly, even in small amounts.

Your emergency fund is your financial seatbelt. It might not feel exciting, but when you need it, you’ll be grateful it’s there.

Step 4: Tackle Your Debt—Strategically

Debt isn’t always bad. A mortgage or a business loan can be smart tools for growth. But high-interest credit card debt? That’s where things get risky.

Start by identifying all your debts:

- Credit cards

- Student loans

- Auto loans

- Buy-now-pay-later services

Use either the snowball method (start with the smallest balance) or the avalanche method (start with the highest interest rate). Whichever motivates you most, stick with it.

Avoid accumulating new debt during this time, and always pay more than the minimum when possible.

Step 5: Start Investing—Even If It’s Just a Little

Once you’ve got control of your spending and debt, it’s time to make your money work for you. That’s what investing is all about.

Investing isn’t only for the rich—it’s for anyone who wants to grow their money over time. Whether it’s through index funds, retirement accounts, or real estate, compound interest can be your best friend.

But here’s the golden rule: don’t invest in what you don’t understand. Take time to research. Consider your risk tolerance. And start small if needed.

If you feel overwhelmed, consult a certified financial planner. Even one meeting can provide clarity that lasts for years.

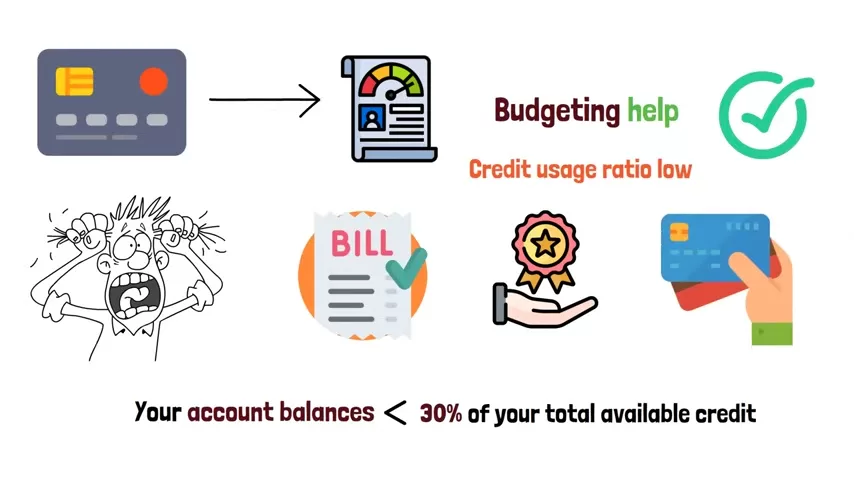

Step 6: Manage Credit Wisely

Credit is a tool, not a lifestyle. When used wisely, it can help you build a strong credit score, qualify for better loans, and even earn rewards. When abused, it leads to stress, debt, and long-term damage.

Best practices:

- Never spend more than you can pay off monthly

- Keep your credit utilization under 30%

- Pay on time, every time

- Review your credit report annually

If credit cards tend to tempt you, consider freezing them or switching to a debit card until your financial discipline improves.

Step 7: Think Beyond Yourself — Protect Your Family

Personal finance isn’t just about the present—it’s about building a future for those you care about. That means thinking about life insurance, estate planning, and how your family would manage financially if something happened to you.

Set up a will. Consider trusts. Review your insurance coverage. It may feel like a morbid task, but preparing now is one of the greatest gifts you can leave your loved ones.

Step 8: Don’t Forget to Enjoy Life

All work and no play? That’s a fast track to burnout. The purpose of managing your finances isn’t to live in constant restriction—it’s to free yourself from financial anxiety.

Give yourself permission to spend on things that bring you joy—whether that’s travel, hobbies, or the occasional night out. Just do so intentionally, not impulsively.

Money should serve your life, not the other way around.

Final Thoughts

Mastering money is not about perfection—it’s about consistency. It’s not reserved for the wealthy or the financially gifted. Everyone, from students to entrepreneurs, can benefit from understanding and applying the personal finance basics.

Start where you are. Learn as you go. And most importantly, take action.

Because when you understand how money works, you don’t just change your bank account—you change your life.